What is APR on a Credit Card? Simple Guide for Beginners

Adman Brooks

Monday, September 8, 2025 at 11:35 PM EDT

Understanding APR on a credit card is the first step to smart borrowing. Many beginners see the term and feel insecure, but it is explained. Apr, or annual percentage rate, is the real cost of borrowing on your credit card. Knowing how credit card APR works helps you manage payments, avoid high interest rates, and make better financial decisions.

APR on a credit card affects each purchase if you do not pay in full. The higher the APR, the more interest you will pay over time. By learning how credit card is calculated, you can plan your payments carefully. With the right approach, you can use your card effectively without falling into expensive debt.

What does APR mean on a credit card?

Apr stands for the annual percentage. It represents the annual cost of borrowing money with your credit card. This rate is shown as a percentage. If you keep a balance instead of paying in full, the bank uses APR to calculate how much interest you owe.

Think of April as the “price tag” on your credit card. Just as a product has a price, it also has a cost of borrowing money. Apr shows the price over one year. For example, if your card has a 20% April, it means you can pay 20% of the balance in interest if you don’t pay it.

Apr is different from just one interest rate. An interest rate often excludes fees. Apr may contain certain fees, making it a better measure of the real costs of loans.

How does APR work?

The APR works by charging interest on its unpaid balance. If you buy something and do not pay the full bill, what is left to the Apr. The bank performs this daily calculation and adds interest to your balance.

Suppose your card has 24% APR. This means that the daily interest rate is about 0.066%. If you pay $ 1,000 and keep it for a month, the interest will be added daily. By the end of the month, you will pay approximately $ 20 more. In more than a year, it can become hundreds of dollars.

This is the reason that the balance on the high-April card is expensive. Even small balances grow quickly. The longer you leave it unpaid, the more you spend on interest.

Do I pay APR if I pay my balance in full?

No, not usually. Most credit cards have an interest-free period. This is the time between the date of purchase and the due date for payment. If you pay the full balance within that period, you will not pay interest. For example, if you spend $ 500 this month and pay it by the due date, no APR.

But if you only pay $ 100, the remaining $ 400 will collect interest. Paying in full every month is the best way to avoid APR completely. It’s like using the card for free, as long as you manage your payments.

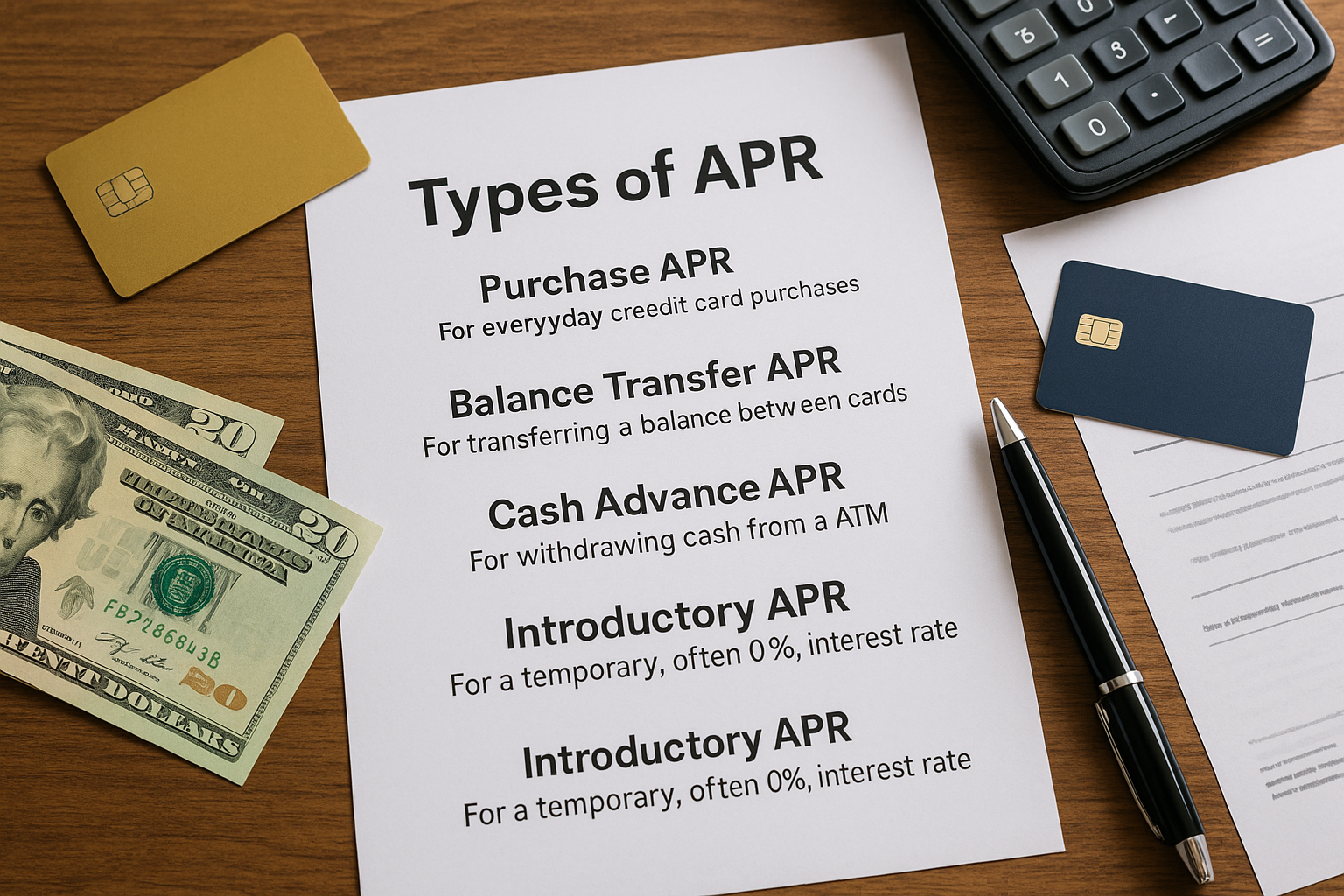

Types of APR on a Credit Card

Credit cards not only have an April. Instead, they often come with several prices depending on how to use the card. The most common are purchases of April, balance transfer of April, and cash advance of April. Some cards also offer an introductory APRs that start at 0% for a limited period. In some cases, a penalty APR may apply if you miss payments or break short-term.

Purchase APR

The purchase of an APR is the most common type. This applies when you buy something with your credit card, such as groceries, gas or clothing. If you pay your full balance by the due date every month, you usually do not owe any interest thanks to the repayment period. But if you have a balance, this APR kicks in, and interest will begin to build on what remains unpaid.

Balance Transfer APR

This APR applies whilst you circulate debt from one card to another. Many credit score playing cards provide promotional balance switch APRs, frequently 0% for a fixed length like 12 to 21 months. This can be a useful way to pay down debt without piling up. However, balance transfers frequently consist of a switch fee, commonly 3% to 5% of the amount transferred. Once the intro duration ends, the normal stability switch APR applies, which is frequently just like or higher than the acquisition APR.

Cash Advance APR

A cash advance occurs when you use your credit card to extract cash from an ATM or a bank. Cash is almost always higher than purchasing the APRS for advances, and the interest begins immediately – there is no grace period. At its top, most issuers add a cash advance fee, such as $ 10 or 5% withdrawal, whichever is more. Due to these costs, cash is one of the most expensive ways to borrow money, with advance credit cards.

Introductory APR

Many credit cards provide a low or 0% introductory APR for a limited time, frequently 6 to 21 months. This can apply to purchases, balance transfers, or both. Introductory APRs are designed to attract new customers and may be a great possibility to finance huge purchases or consolidate debt without paying interest for a while. It’s critical to observe when the introductory duration ends, because as soon as it does, the normal APR will apply to any remaining balance.

Penalty APR (extra one worth noting)

Some cards also have a penalty APR. This high rate can be triggered if you pay late or break other conditions of your agreement. Penalty APRS can be much higher than your regular APR, sometimes above 29%. Not all cards apply it, but when they do, the increased rate may remain monthly or even indefinitely.

Why is APR important?

APR is important because it affects how much you actually pay when using your card. If you carry the remaining amount, a low APR saves you money. High APR borrowing is very expensive. Imagine two people with the same $ 1,000 balance. One has 15% APR, the other 25%. After a year, the first pays around $ 150 in interest, while the second pays $ 250. This is a difference of $ 100 for the same purchase.

When comparing the credit cards, the APR is one of the most important numbers to view. Awards and allowances are helpful, but interest costs can easily beat them if you do not make full payments.

How do banks calculate APR charges?

Banks don’t wait till the quit of the yr to apply APR. Instead, they calculate it day by day. They take the APR, divide it with the aid of 365, and get the daily fee. Then they observe that in your stability. For example, with a 20% APR, the day-by-day fee is 0.0.5%. If you’ve got a $500 stability, each day you’ll upload about 28 cents in hobby. Over a month, that adds up to around $eight.40.

This daily calculation makes the hobby grow speedily. Even if you make a payment, the financial institution may still charge interest on the balance until it’s completely cleared.

What is a good APR for a credit card?

A good APR depends on your credit history. People with excellent credit scores can qualify for cards with less than 15%APRS. People with average credit often see APRS between 18% and 24%. For poor credit, APRS can go above 25%.

No single “best” is not April, but lower, better. If you plan to carry the remaining amount, you may be smart to find a card with the lowest APR. If you always make full payments, the APR matters less, but it still provides a safety trap if you can never.

Can APR change over time?

Yes, the Apr can change. Many credit cards contain variable APRS. This means that they are tied to an index like the prime rate. When the index changes, your APR also changes. For example, if the prime rate increases by 1%, your credit card APR may also increase by 1%. It makes borrowing more expensive.

Some cards also increase your APR if you remember the payment. This is called penalty APR, and it can be much higher than your normal rate. Lenders use it to reduce their risk and encourage timely payments. Over time, your APR can also be affected by your credit score, overall loan, and your issuer’s set terms.

How Can You Avoid Paying APR on a Credit Card?

The best way to avoid paying APR is to pay your remaining amount every month. It prevents interest from construction at any time. If you cannot make a full payment, try to pay more than the minimum. The faster you pay the remaining amount, the lower the interest you will pay.

Another option is to use a 0% introductory APR card. These borrow you without interest for a scheduled time. This is helpful if you need to spread payments on a large purchase. Budgets and reminders also help. Automatic payment ensures that you never miss the fixed date.

Ultimately, disciplined expenses to avoid APR come down to disciplined expenses and timely payment. Credit cards are most useful when you consider them as a tool, not a source of long-term debt. If you manage your card wisely, you can enjoy the award, create credit, and never pay one percent in interest. Conforming to good habits will keep your finances strong in the long run.

FAQs About Credit Card APR

1. Is the APR charged every month or every year?

Apr is annually, but the banks divide it into a daily price. Interest is added daily if you have a balance.

2. Can I get a 0% APR credit card?

Yes. Many cards offer 0% initial April for a limited period. These are useful for large purchases or balance transfers.

3. Why is the cash post APR higher?

Cash advance is risky for banks. That is why they charge higher interest rates and often have no installment-free period.

4. Do the Apr Credit points affect?

No, April does not even affect your score. But carrying -interest balance can increase debt, which can damage your score.

5. What is better: Low April or more rewards?

It depends on. If you have a balance, a low April is better. If you pay in full monthly, rewards mean more than April.

Trending Insights

Discover the smartest credit card solutions designed to simplify payments and reward your lifestyle